Abstract: The public sector hires

disproportionately more educated workers. Using US microdata, we show

that the education bias also holds within industries and in two thirds

of 3-digit occupations. To rationalize this finding, we propose a model

of private and public employment based on two features. First, alongside

a perfectly competitive private sector, a cost-minimizing government

acts with a wage schedule that does not equate supply and demand.

Second, our economy features heterogeneity across individuals and jobs,

and a simple sorting mechanism that generates underemployment � educated

workers performing unskilled jobs. The equilibrium model is parsimonious

and is calibrated to match key moments of the US public and private

sectors. We find that the public-sector wage differential and excess

underemployment account for 15 percent of the education bias, with the

remaining accounted for by technology. In a counterintuitive fashion, we

find that more wage compression in the public sector raises inequality

in the private sector. A 1 percent increase in unskilled public wages

raises private-sector inequality by 0.13 percent.

Abstract:

In most countries, the public sector

hires dis-proportionally more women than men. We document gender di

erences in employment, transition probabilities, hours, and wages in the

public and private sector using microdata for the United States, the

United Kingdom, France, and Spain. We then build a search and matching

model where men and women decide if to participate and if to enter

private or public sector labor markets. We calibrate our model

separately to the four countries. Running counterfactual experiments, we

quantify whether the selection of women into the public sector is driven

by: (i) lower gender wage gaps, (ii) possibilities of better

conciliation of work and family life, (iii) greater job security, or

(iv) intrinsic preferences for public sector occupations. We find that,

quantitatively, women's higher public sector wage premia and their

preferences for working in the public sector explain most of the

selection. We calculate the monetary value of public sector job security

and work-life balance premia, for both men and women, and we quantify

how wage and employment policies affect male and female unemployment,

inactivity rates, and wages di erently.

Abstract:

The size of the public sector in terms of employment and compensation

has a strong life-cycle dimension. We establish a quantitative

partial-equilibrium life-cycle model with incomplete markets, private

and public sectors, and risk-averse workers, and use it to (i) calculate

three dimensions of public-sector compensation: wage, pension, and

job-security premia, and (ii) quantify the effects of harmonizing the

compensation in the two sectors. We find that the job-security and

pension�s premia are important forms of compensation to public-sector

workers. Harmonizing the characteristics of public employment with those

of the private sector would lower the unemployment rate and reduce

government costs.

Abstract: We set up a search and matching model

with a private and a public sector to understand the effects of

employment and wage policies in the public sector on unemployment and

education decisions. The effects of wages and employment of skilled and

unskilled public-sector workers on the educational composition of the

labor force depend crucially on the structure of the labor market. An

increase of skilled public-sector wages has a small positive impact on

educational composition and larger negative impact on the private

employment of skilled workers, if the two sectors are segmented. If

search across the two sectors is random, it has a large positive impact

on education and a large positive impact on skilled private employment.

We highlight the usefulness of the model for policymakers by calculating

the value of public-sector job security for skilled and unskilled

workers.

Abstract: We set up a model with search and

matching frictions to understand the effects of employment and wage

policies, as well as nepotism in hiring in the public sector, on

unemployment and rent seeking. Conditional on inefficiently high

public-sector wages, more nepotism in public sector hiring lowers the

unemployment rate because it limits the size of queues for public-sector

jobs. Wage and employment policies impose an endogenous constraint on

the number of workers the government can hire through connections.

Abstract: We measure the size of gross

worker flows between public and private sector and their importance for

the dynamics of public employment over the last two decades in the US,

UK, France and Spain. Between 10 and 35 percent of all in flows and out

flows of the public sector are from and to private employment. These

flows only account for 7 to 25 percent of the fluctuations of public

employment.

Abstract: For the period between 2003 and

2018, we document a number of facts about worker gross flows in France,

the United Kingdom, Spain and the United States, focussing on the role

of the public sector. Using the French, Spanish and UK Labour Force

Survey and the US Current Population Survey data, we examine the size

and cyclicality of the flows and transition probabilities between

private and public employment, unemployment and inactivity. We examine

the stocks and flows by gender, age and education. We decompose

contributions of private and public job-finding and job-separation rates

to fluctuations in the unemployment rate. Public-sector employment

contributes 20 percent to fluctuations in the unemployment rate in the

UK, 15 percent in France and 10 percent in Spain and the US.

Private-sector workers would forgo 0.5 to 2.9 percent of their wage to

have the same job security as public-sector workers.

Abstract:

Countries with a lower fraction of workers with secondary

education have smaller firms. We set up a model of occupational choice

where individuals have primary, secondary or tertiary education. A more

educated work force raises firm size and productivity. More educated

workers earn higher wages, and hence among educated individuals only the

more able become entrepreneurs. We find that within the framework of our

model, different educational attainments can explain one third of the

difference in average firm size between the US and Mexico. While

improved educational attainments hence imply an increase in firm size

over time, a fall in the price of capital together with capital-skill

complementarity acts in the opposite direction, something that can

explain a relatively constant average firm size in the US since the late

1970's. Our policy experiments highlight additional effects of public

employment and a skill bias in public hiring on firm size and

productivity.

Abstract:I propose a reform of public sector wages

consisting of: i) a review of pay of all public sector workers to align

the distribution of public sector wages with the private sector and ii)

stipulating up a rule to determine the yearly growth rate of public

sector wages. I use a model with search and matching frictions and

heterogeneous workers to evaluate this reform in the steady-state and

over the business cycle. The model was calibrated to the UK economy

based on Labour Force Survey data. A review of the pay received by all

public sector workers to align the distribution of wages with the

private sector reduces steady-state unemployment by 3 percentage points.

Implementing a procyclical simple rule to determine the yearly growth

rate of public sector wages reduces the volatility of unemployment by 3

to 8 percent and of private consumption by 4 to 12 percent. I show that,

in a sample of 29 developed countries for the pre-crisis period of

1995-2006, countries that deviated more from the rule had a larger

increase in the unemployment rate and higher volatility of unemployment

relative to GDP.

Abstract:

A model with search and matching frictions and heterogeneous workers was

established to evaluate a reform of the public sector wage policy in

steady-state. The model was calibrated to the UK economy based on Labour

Force Survey data. A review of the pay received by all public sector

workers to align the distribution of wages with the private sector

reduces steady-state unemployment by 1.9 percentage points.

Abstract:I build a dynamic stochastic general

equilibrium model with search and matching frictions in order to

determine the optimal public sector wage policy. Public sector wages are

crucial to achieve efficient allocation of jobs. High wages induce too

many unemployed to queue for public sector jobs, in turn raising

unemployment. The optimal wage depends on the frictions in the two

sectors. Following technology shocks, public sector wages should be

procyclical, and deviations from the optimal policy significantly

increase the volatility of unemployment.

Awarded the Austin Robinson Memorial Prize for the best paper published

in the Economic Journal in 2015 by an author who is within five years of

receiving their PhD.

Abstract:We examine the

interactions between public and private sector wages per employee in

OECD countries. The growth of public sector wages and of public sector

employment positively affects the growth of private sector wages.

Moreover, total factor productivity, the unemployment rate and the

degree of urbanisation are also important determinants of private sector

wage growth. With respect to public sector wage growth, we find that it

is influenced by fiscal conditions in addition to private sector wages.

We then set up a dynamic labour market equilibrium model with two

sectors, search and matching frictions and exogenous growth to

understand the transmission mechanisms of fiscal policy. The model is

quantitative consistent with the main estimation findings.

Abstract:I argue that when two

or more credit rating agencies rate a product, they have the incentive

to put a weight on the competitors' rating. This piggybacking allows an

agency to increase the precision of its own rating while doing less

monitoring. Although it is privately effcient, it implies that having

more rating agencies does not necessarily increase the overall

monitoring. Using annual data on sovereign debt ratings I show that the

probability of a rating change depends on the rating differential

towards its competitors, even when accounting for a common information

set, which is consistent with the hypothesis.

Abstract:The reaction of EU bond and equity market

volatilities to sovereign rating announcements (Standard & Poor's,

Moody's, and Fitch) is investigated using a panel of daily stock market

and sovereign bond returns. The parametric volatilities are filtered

using EGARCH specifications. The estimation results show that upgrades

do not have significant effects on volatility, but downgrades increase

stock and bond market volatility. Contagion is present, with sovereign

rating announcements creating interdependence among European financial

markets with upgrades (downgrades) in one country leading to a decrease

(increase) in volatility in other countries. The empirical results show

also a financial gain and risk (value-at-risk) reduction for portfolio

returns when taking into account sovereign credit ratings� information

for volatility modelling, with financial gains decreasing with higher

risk aversion.

Abstract:We use EU sovereign

bond yield and CDS spreads

daily

data to

carry out an event study analysis on

the

reaction of government yield spreads before and after announcements from rating

agencies (Standard & Poor's, Moody's, Fitch). Our results show significant

responses of government bond yield spreads to changes in rating notations and

outlook, particularly in the case of negative announcements. Announcements are

not anticipated at 1-2 months horizon but there is bi-directional causality

between ratings and spreads within 1-2 weeks; spillover effects especially among

EMU countries and from lower rated countries to higher rated countries; and

persistence effects for recently downgraded countries.

Abstract:We use sovereign

debt rating estimations from Afonso, Gomes and Rother (2009, 2011) for Fitch,

Moody's, and Standard & Poor's, to assess to what extent the recent fiscal

imbalances are being reflected on the sovereign debt notations. With macro and

fiscal data up to 2010, and macro and fiscal projections, we obtain the expected

rating for several OECD countries. The answer to the title question is yes, but

in a diverse way for each country. Our average model predictions point to a

heterogeneous behaviour of rating agencies across countries.

Abstract:

We study the determinants of sovereign debt ratings from the three main

international rating agencies, for the period 1995-2005. Using linear and

ordered response models we employ a specification that allows us to distinguish

between short and long-run effects, on a country's rating, of macroeconomic and

fiscal variables. Changes in GDP per capita, GDP growth, government debt, and

government balance have a short-run impact on a country's credit rating, while

government effectiveness, external debt, foreign reserves and default history

are important long-run determinants.

Abstract:

Using ordered logit and probit plus random effects ordered probit approaches we study the

determinants of sovereign ratings. The last procedure should be more appropriate

for panel data as it considers the existence of an additional normally

distributed cross-section error.

Abstract: The public sector hires

disproportionately more educated workers. Using US microdata, we show

that the education bias also holds within industries and in two thirds

of 3-digit occupations. To rationalize this finding, we propose a model

of private and public employment based on two features. First, alongside

a perfectly competitive private sector, a cost-minimizing government

acts with a wage schedule that does not equate supply and demand.

Second, our economy features heterogeneity across individuals and jobs,

and a simple sorting mechanism that generates underemployment � educated

workers performing unskilled jobs. The equilibrium model is parsimonious

and is calibrated to match key moments of the US public and private

sectors. We find that the public-sector wage differential and excess

underemployment account for 15 percent of the education bias, with the

remaining accounted for by technology. In a counterintuitive fashion, we

find that more wage compression in the public sector raises inequality

in the private sector. A 1 percent increase in unskilled public wages

raises private-sector inequality by 0.13 percent.

Abstract:

We propose a simple theory of under-

and over-employment. Individuals of high type can perform both skilled

and unskilled jobs, but only a fraction of low-type workers can perform

skilled jobs. People have different non-pecuniary values over these

jobs, akin to a Roy model. We calibrate two versions of the model to

match moments of 17 OECD economies, considering separately education and

skills mismatch. The cost of mismatch is 3% of output on average but

varies between -1% to 9% across countries. The key variable that

explains the output cost of mismatch is not the percentage of mismatched

workers but their wage relative to well-matched workers.

Abstract:

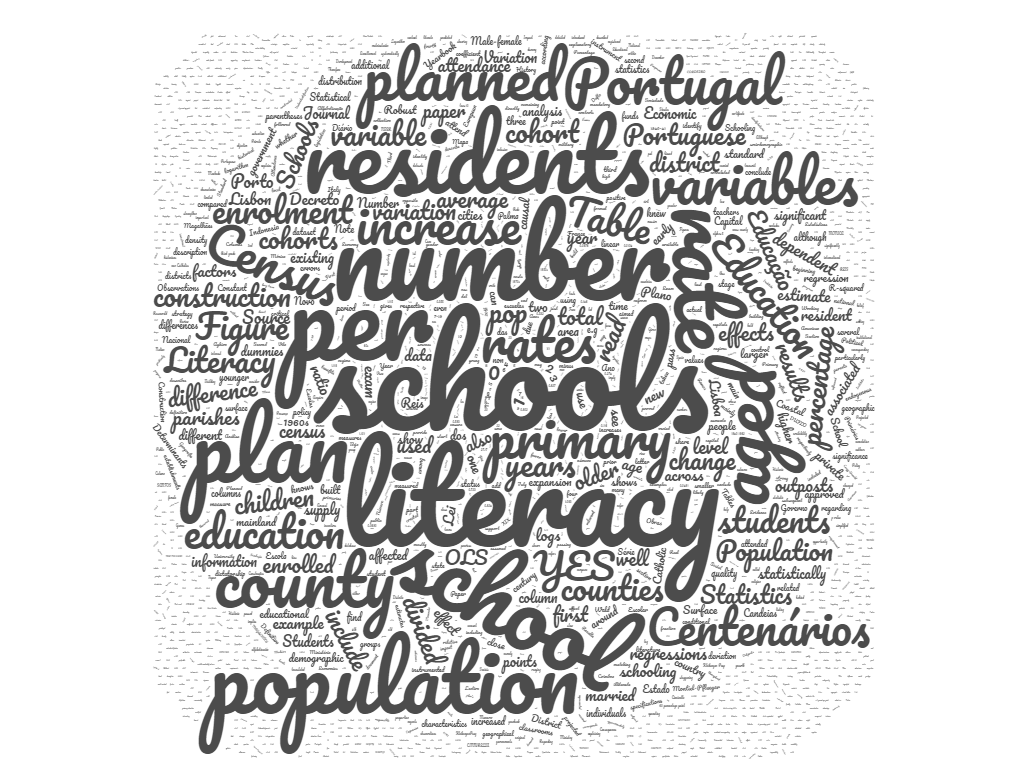

In 1940, the Portuguese government approved a massive primary school

construction plan that projected a 60% increase in the number of primary

schools. Based on the collection of a new dataset, we describe literacy

levels in Portugal prior to the plan as well as the plan�s strategy

regarding the location of schools. We then estimate the causal impact of

the increase in the number of schools between 1940 and the early 60s on

enrolment and literacy, all at the county level. We conclude the

increase in the number of schools was responsible for 80% of the

increase in enrolment and 13% of the increase in the literacy rate of

the affected cohorts.

Abstract: We set up a search and matching model

with a private and a public sector to understand the effects of

employment and wage policies in the public sector on unemployment and

education decisions. The effects of wages and employment of skilled and

unskilled public-sector workers on the educational composition of the

labor force depend crucially on the structure of the labor market. An

increase of skilled public-sector wages has a small positive impact on

educational composition and larger negative impact on the private

employment of skilled workers, if the two sectors are segmented. If

search across the two sectors is random, it has a large positive impact

on education and a large positive impact on skilled private employment.

We highlight the usefulness of the model for policymakers by calculating

the value of public-sector job security for skilled and unskilled

workers.

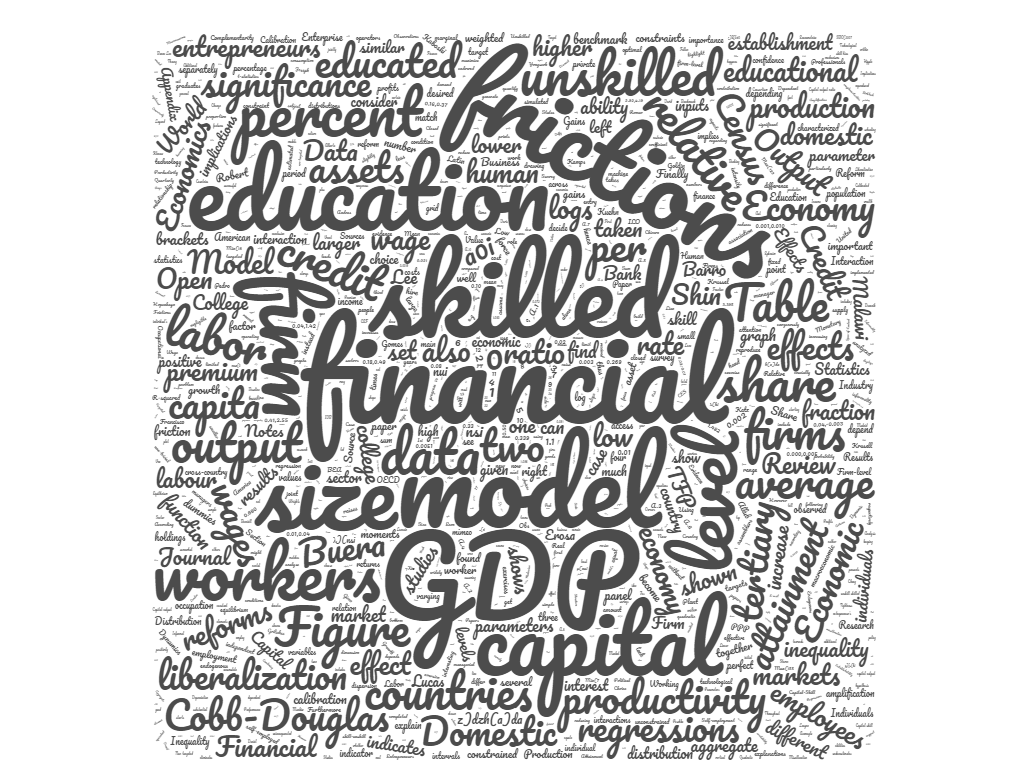

Abstract: Capital-skill complementarity

in production implies non-trivial interactions between availability of

human capital and financial constraints. Firms that are constrained in

their access to finance hire a lower proportion of skilled workers

compared to unconstrained rms. On the other hand, a lack of human

capital increases skilled wages, reducing firms' desired capital

intensity and thus loosening effective financial constraints. We build a

dynamic occupational-choice model to quantify how a lack of human

capital and financial frictions, as well as the joint effect of both

restrictions interact to explain cross-country differences in aggregate

output per capita, productivity, average firm size, and college premia.

We calibrate our model to US data, and we vary financial frictions and

educational attainment as observed across countries. We find that the

joint effect of both restrictions is up to 50 percent larger compared to

the sum of the individual effects. In countries with a negligible share

of tertiary educated workers, financial development has only small

effects on aggregate output.

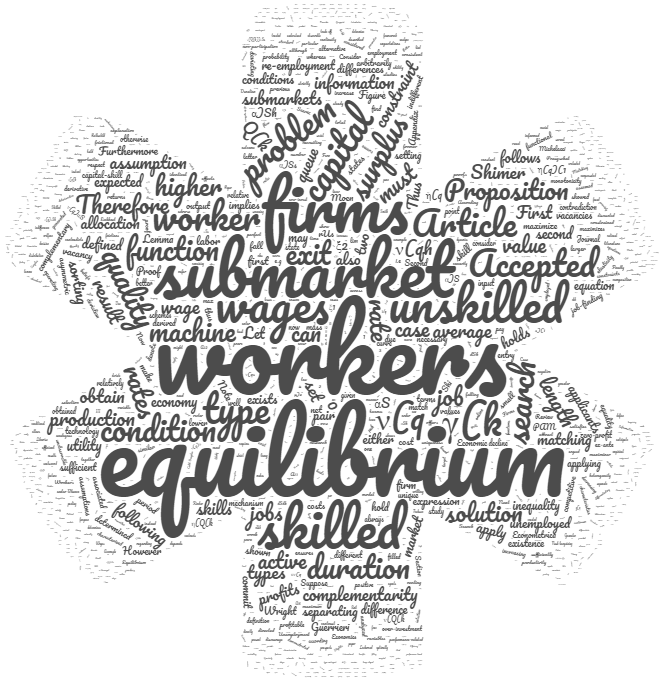

Abstract:Exit rates from unemployment and re-employment wages

decline over an unemployment period after controlling for worker

observable characteristics. In this study, the role of unobserved

heterogeneity in an economy where workers are informed privately about

skills and they direct their own search is investigated. We show that

the unique equilibrium is separating and that skilled workers have more

job opportunities with higher wages. The composition of the unemployment

pool varies with the duration of unemployment, so the average exit rates

and wages fall with time. The separating equilibrium relies on the

ability of firms to commit to renting an input that is complementary in

terms of production to the skills of worker and performance-related pay

schemes.

Abstract:

Countries with a lower fraction of workers with secondary

education have smaller firms. We set up a model of occupational choice

where individuals have primary, secondary or tertiary education. A more

educated work force raises firm size and productivity. More educated

workers earn higher wages, and hence among educated individuals only the

more able become entrepreneurs. We find that within the framework of our

model, different educational attainments can explain one third of the

difference in average firm size between the US and Mexico. While

improved educational attainments hence imply an increase in firm size

over time, a fall in the price of capital together with capital-skill

complementarity acts in the opposite direction, something that can

explain a relatively constant average firm size in the US since the late

1970's. Our policy experiments highlight additional effects of public

employment and a skill bias in public hiring on firm size and

productivity.

Abstract:

A model with search and matching frictions and heterogeneous workers was

established to evaluate a reform of the public sector wage policy in

steady-state. The model was calibrated to the UK economy based on Labour

Force Survey data. A review of the pay received by all public sector

workers to align the distribution of wages with the private sector

reduces steady-state unemployment by 1.9 percentage points.

Abstract: We measure the size of gross

worker flows between public and private sector and their importance for

the dynamics of public employment over the last two decades in the US,

UK, France and Spain. Between 10 and 35 percent of all in flows and out

flows of the public sector are from and to private employment. These

flows only account for 7 to 25 percent of the fluctuations of public

employment.

Abstract: For the period between 2003 and

2018, we document a number of facts about worker gross flows in France,

the United Kingdom, Spain and the United States, focussing on the role

of the public sector. Using the French, Spanish and UK Labour Force

Survey and the US Current Population Survey data, we examine the size

and cyclicality of the flows and transition probabilities between

private and public employment, unemployment and inactivity. We examine

the stocks and flows by gender, age and education. We decompose

contributions of private and public job-finding and job-separation rates

to fluctuations in the unemployment rate. Public-sector employment

contributes 20 percent to fluctuations in the unemployment rate in the

UK, 15 percent in France and 10 percent in Spain and the US.

Private-sector workers would forgo 0.5 to 2.9 percent of their wage to

have the same job security as public-sector workers.

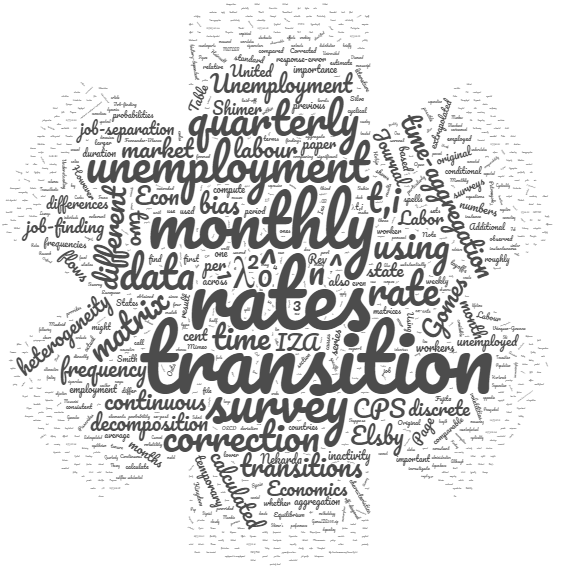

Abstract:Labour markets transition rates are

typically estimated using survey data, which are mainly carried at

monthly or quarterly frequency. I argue that rates from surveys at

different frequencies are not comparable, even if corrected for time

aggregation. I estimate labour market transition rates using monthly and

quarterly frequency CPS data. I apply time-aggregation correction to

make them comparable. I find notable differences in terms of levels and

volatilities. While the continuous time-aggregation correction does not

alter the unemployment decomposition using the monthly survey, it does

so when using the quarterly survey.

Abstract:

This paper documents a number of facts about worker gross flows in the United

Kingdom for the period between 1993 and 2010. Using Labour Force Survey data, I

examine the size and cyclicality of the flows and transition probabilities

between employment, unemployment and inactivity, from several angles. I examine

aggregate conditional transition probabilities, job-to-job flows, employment

separations by reason, flows between inactivity and the labour force and flows

by education. I decompose contributions of job-finding and job-separation rates

to fluctuations in the unemployment rate. Over the past cycle, the

job-separation rate has been as relevant as the job-finding rate.

Abstract: We show that, in a financially

constrained environment, relative to an active fiscal--passive monetary

policy regime, an active monetary--passive fiscal policy amplifies

technology shocks, neutralizes financial shocks, and mitigates the

expansionary effects of fiscal shocks through a ``debt deflation" and

``real interest rate" channels. Several features of the data suggest

that, during the last decade, the United States implemented an active

fiscal--passive monetary policy, while the Euro area implemented an

active monetary--passive fiscal policy, implying that the distinct

post-crisis dynamics of the United States and the Euro area can be

rationalized through different fiscal and monetary policy mixes.

Abstract:

Over the past 40 years public investment has declined in

most developed countries. This paper argues that such pattern can be the

consequence of investment-specific technological progress. Public

investment, mostly on infrastructures, experienced a slower rate of

innovation than private investment, composed primarily by equipment and

software. Within a simple neoclassical growth model with a public

sector, we show that such type of technological progress reduces the

incentives to invest in public capital, and accounts for 80 percent of

the observed decline. The implied co-movements of other fiscal

instruments are also consistent with observed trends.

Abstract: We measure the regional impact of the European Capital of Culture

programme using a difference-in-differences approach. We compare the

regions of cities that hosted the

event with the regions of cities that tried to host it but did not

succeed. GDP per capita in hosting regions is 4.5 percent higher

compared to non-hosting regions during the event and the effect persists

more than 5 years after it. This result suggests that the economic

dimension of the event is important and support claims that the event

serves as catalyst for urban regeneration and development.

Abstract:

We show, in a broad class of affine general equilibrium models with

long-run risk, that the covariances between asset returns are linear

functions of risk factors. We use a dynamic conditional correlation

model to measure the covariances of stock and sovereign bond markets in

the Euro Area. We use a new approach to measure risk factors based on

Google search data. The factors explain 50 to 60 percent of the

variation of the covariances between European stocks and 25 to 35

percent of the covariances between European bonds. The information

improves the portfolio performance compared to an equally weighted

portfolio.